Photo by Richard Hurd

Metro Metrics November 2025

Metro Metrics is a monthly data snapshot that explores key economic indicators reflecting the health of the Madison metro economy.

The Next Normal for Greater Madison

Since 2024, the Chamber, in coordination with several partner organizations, has conducted an annual survey of regional employers to assess current and projected economic conditions. These surveys are designed to help us understand the Next Normal (N²) for work and workplaces in our region.

This year’s survey received responses from 241 unique businesses representing 20 different industries. Topline results and partner perspectives were shared at a recent Chamber Lunch(UP)date, which can be viewed here. For this month’s Metro Metrics, we take a closer look at the data to assess trends and peer metro comparisons.

Business Indicators

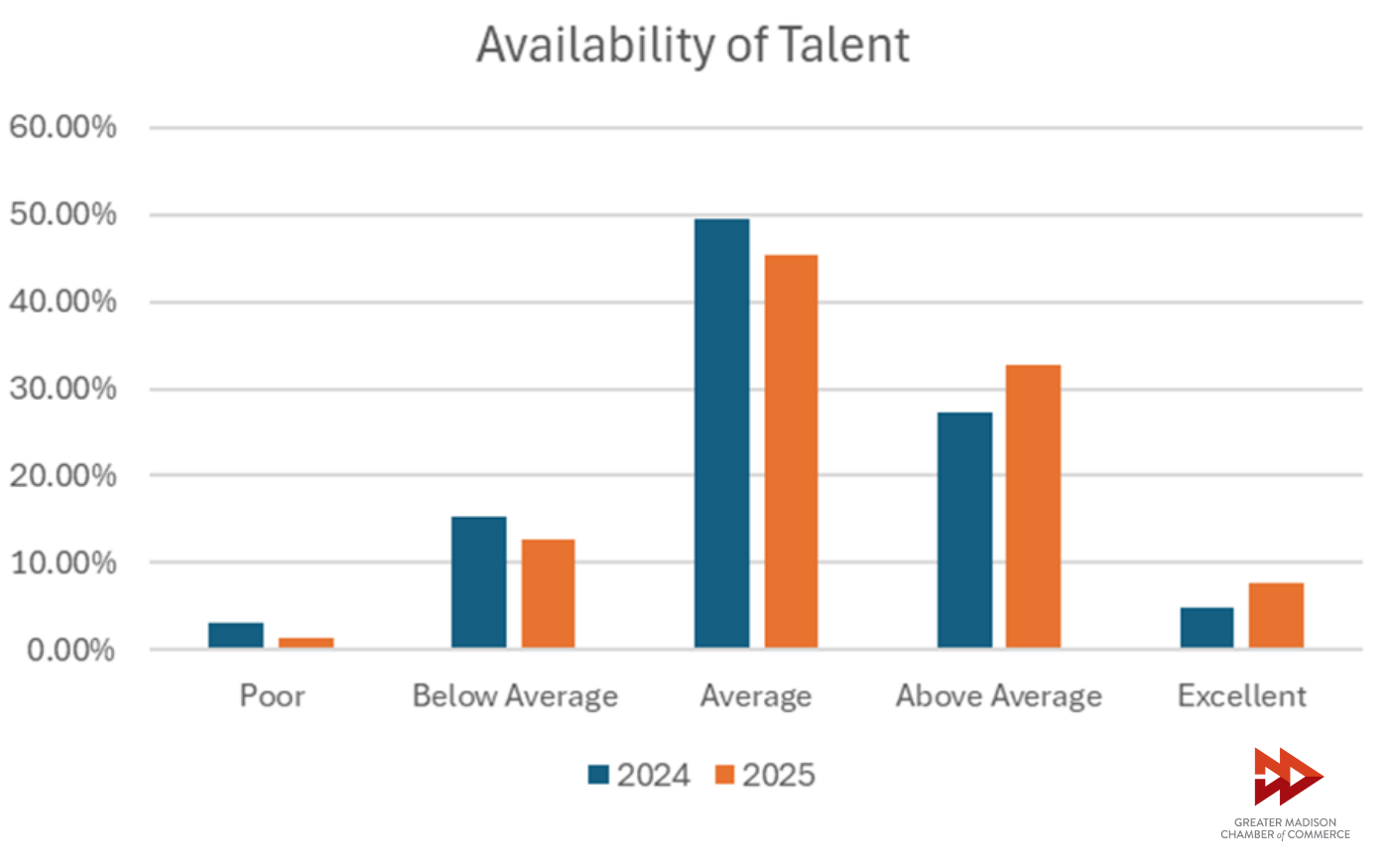

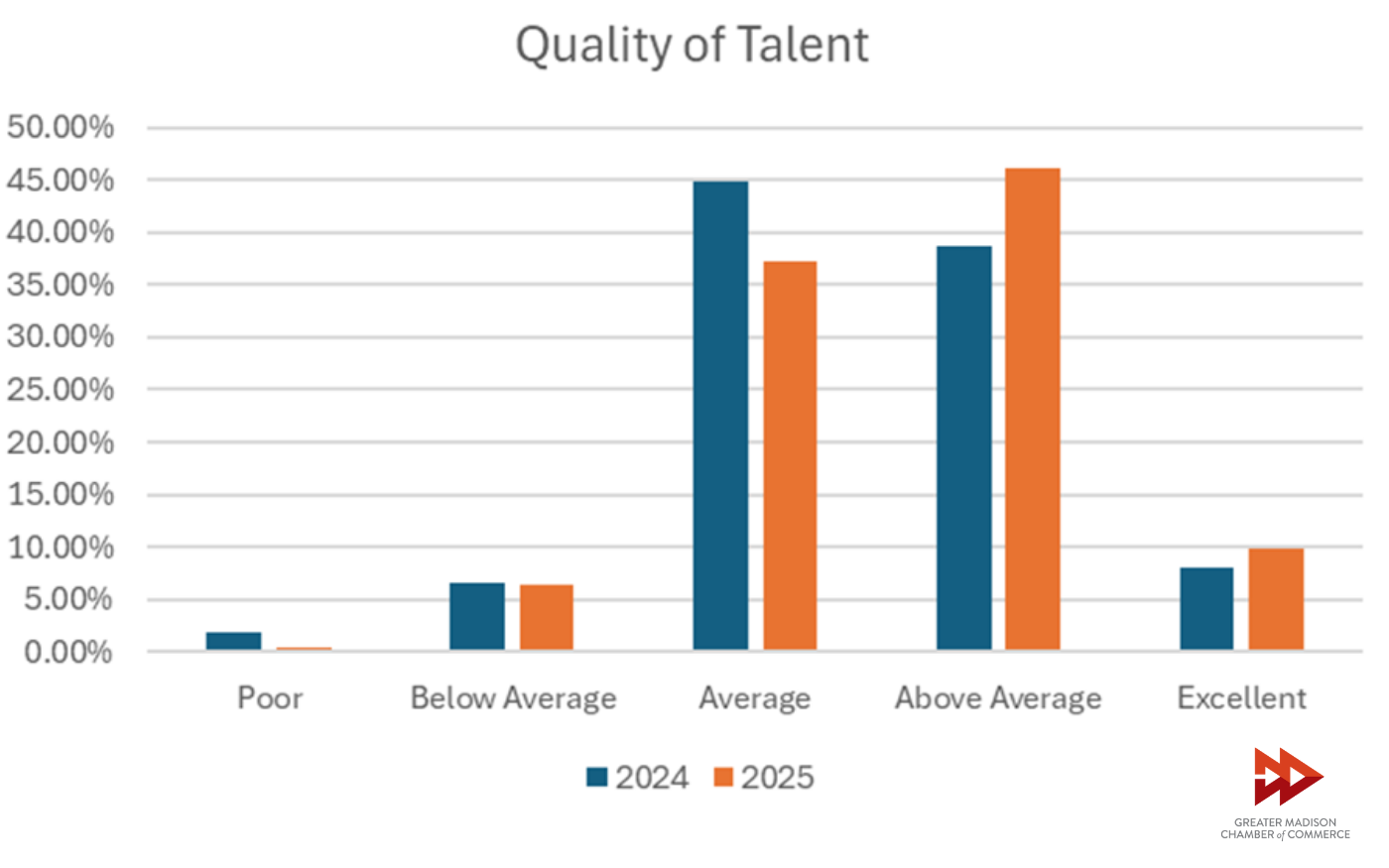

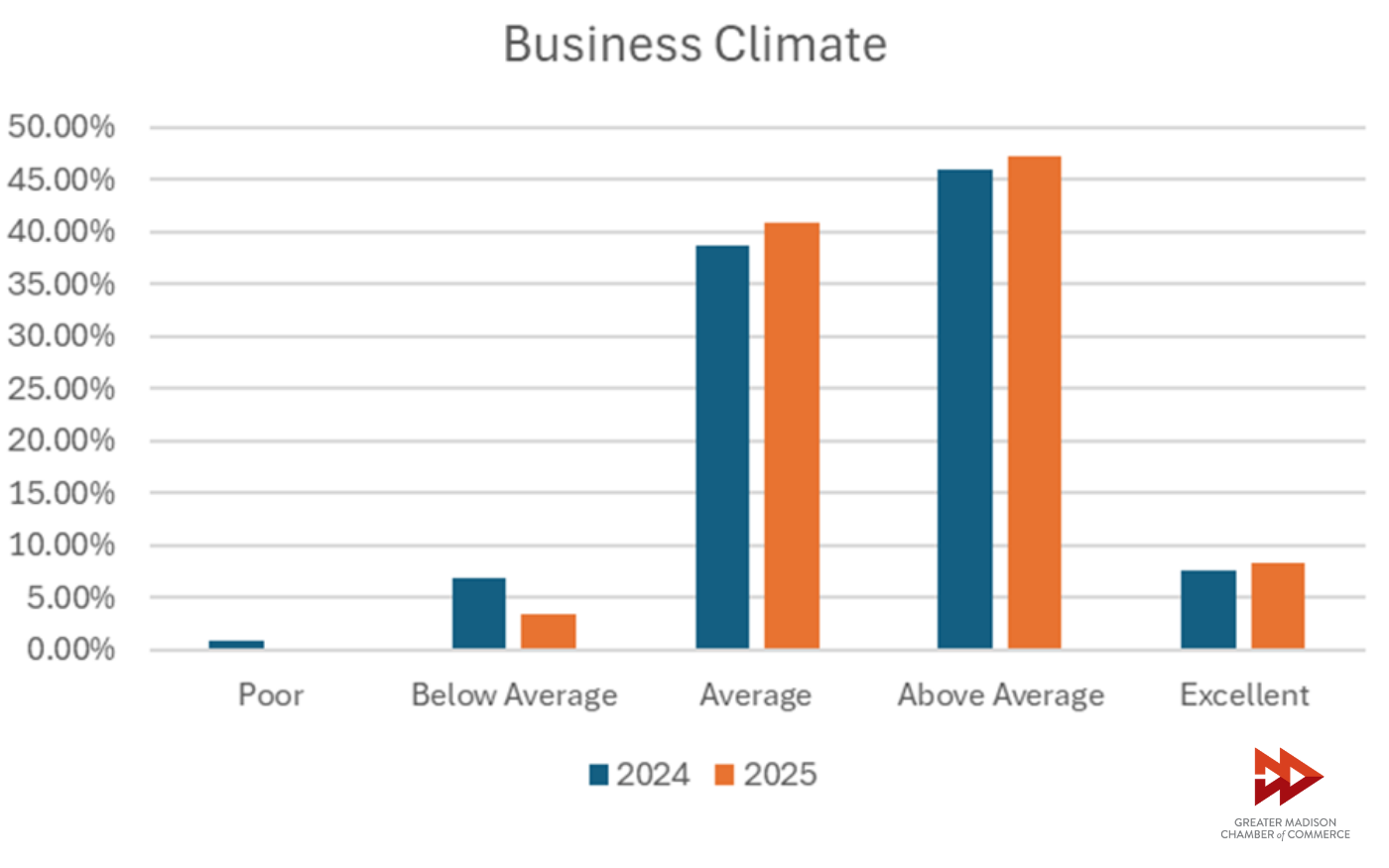

There were many encouraging results for both the availability (Fig. 1) and quality of talent (Fig. 2), with both metrics showing increases in the proportion of businesses that reported them as “average” or better compared to last year’s survey. Similar increases were found in respondent views on the region’s business climate (Fig. 3).

The distribution of responses to these business indicators is shown below. A consistent pattern can be observed in all three measurements. The proportion of businesses that rated these indicators “poor” or “below average” always drops from 2024 to 2025 and the proportion that rated them “above average” or “excellent” always rises. The proportion that rated the indicators “average” either increased or decreased, depending on the indicator. This shows that the improvement isn’t just due to ratings trending towards the middle but that businesses are rating them higher.

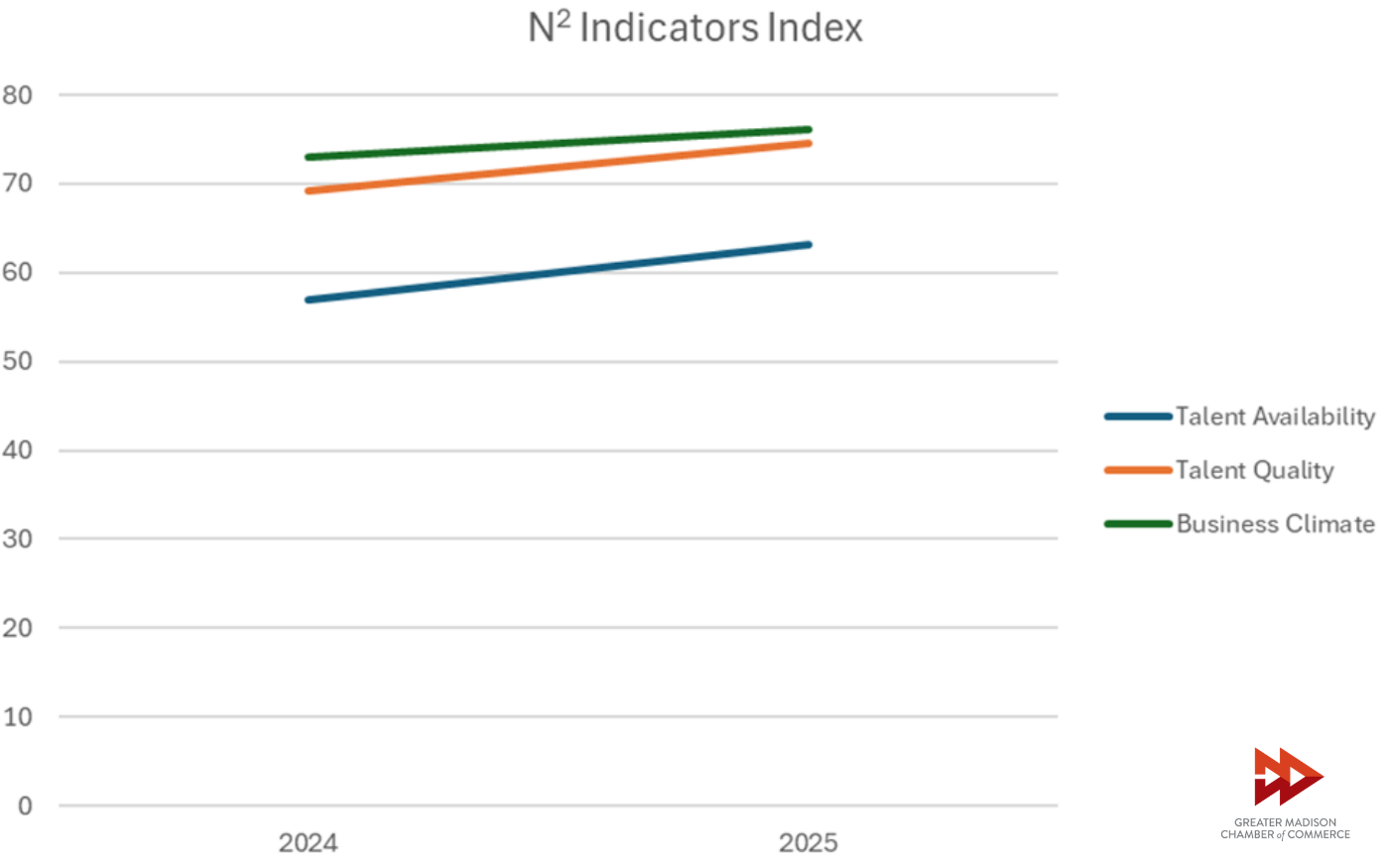

Another way to visualize and understand the difference between 2024 and 2025 ratings for these indicators is by creating an index (Fig. 4) to measure the difference between how many businesses rated these indicators above average or better and how many rated them below average or worse. The index scales from 0 to 100, with 0 meaning every business rated it negatively, 50 meaning an equal number of businesses rated it positively and negatively and 100 meaning every business rated it positively.

All three indicator indices are above 50 in both survey years, indicating that more businesses felt positively than negatively about the indicators. All three also increased between last year and this year, demonstrating improvement.

How Does Greater Madison Measure Up?

Recently, the U.S. Chamber of Commerce released its 2025 Empowering Small Business Report, which summarizes the results of a national survey of small businesses. The U.S. Chamber defines small businesses as those with fewer than 250 employees, which differs from how the N2 survey categorized businesses. To get the closest approximation for this comparison, we will define Greater Madison’s small businesses as those with fewer than 200 employees.

This year’s Empowering Small Business report focused on AI and how small businesses are using it. According to the report, 40% of small businesses were using AI in 2024, rising to 58% in 2025. AI use among Greater Madison small businesses was 48% in 2024 and 75% in 2025, showing faster AI adoption locally. Similarly, a moderately higher percentage of Greater Madison small businesses are developing custom AI tools compared to the nation.

An additional survey we can use to compare AI trends is McKinsey’s State of AI 2025 report. This report found that although a majority of companies use AI, its use is concentrated in the “experimenting” and “piloting” phases. Just one-third of businesses said their AI use was “scaling” or “fully scaled.” This is similar to the results from N2, where 58% of businesses said that AI was only “minimally integrated” into their workflows.

Tariffs and Uncertainty

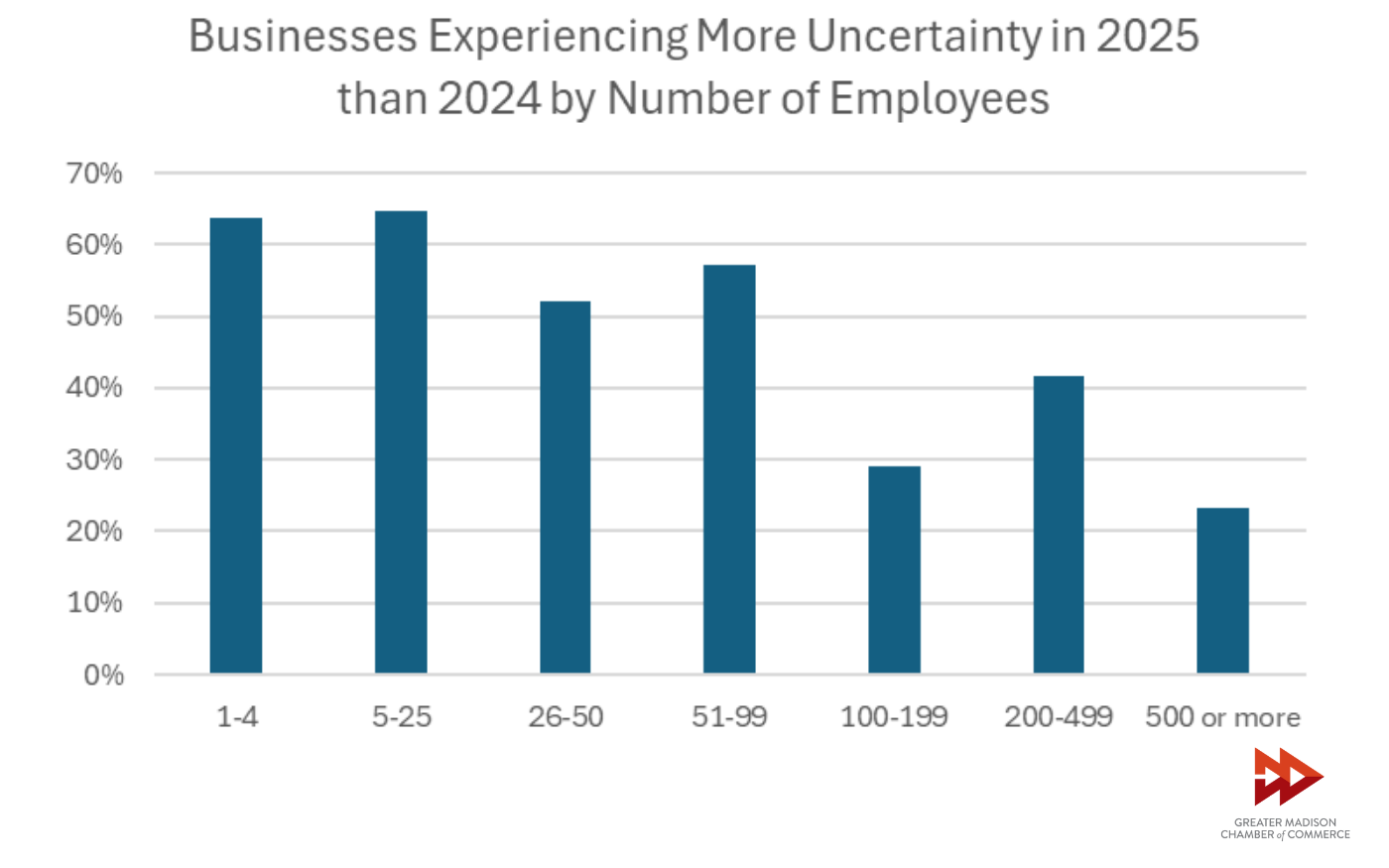

Two significant findings from this year’s survey were the proportion of businesses concerned about tariffs and those facing more uncertainty this year than last year (Fig. 5). The proportion of respondents that listed tariffs as a barrier to their business increased from 5% in 2024, representing the least common barrier, to 36% in 2025, the third-highest barrier. A majority (51%) of surveyed businesses said they were experiencing more uncertainty this year than last year.

The industries most concerned about tariffs this year were retail, advanced manufacturing, arts and entertainment, and construction and trades. While it is not surprising to see industries that are import- or export-dependent identify concerns about trade and tariffs, it is notable that 50% of arts and entertainment businesses that took the survey identified tariffs as a top barrier.

The industries that said they were facing more uncertainty than last year were nonprofit, arts and entertainment, business and professional services, retail, and bioscience. Bioscience employers faced only slightly more uncertainty than the general sample, but because it is a driver industry for the region’s economy, it is worth noting and tracking.

Business size also had a large effect on whether businesses reported facing more uncertainty, with more than 60% of smaller businesses reporting increased levels of uncertainty while less than 30% of larger businesses reported the same.